June 2015, Vol. 70, No.6

Features

HDD In Modern Times

Defining normalcy in the world of horizontal directional drilling has always been virtually impossible.

It started out in the 1980s with big rigs offering a much-needed alternative for large diameter pipeline crossing projects; it quickly evolved into a small rig market that matched perfectly with the telecommunications boom of the 1990s; then faltered mightily with the dawn on the new millennium as the telecom market dove headfirst into a recession and energy navigated through another of its frequent valleys.

But through all the market changes, HDD has survived and prospered. Often described as a “disruptive” technology for underground infrastructure installation, HDD has proven to be a game changer for essentially every market. As the technology recovered from the depressive cycle in the early 2000s, it rapidly spread into other niches, carving out a strong market segment and proving that HDD had become a reliable, high-quality and affordable technology.

This information and much more are detailed in the 17th Annual Underground Construction 2015 HDD Survey of the U.S. market. This exclusive industry research was conducted during March and April. Surveys were sent via both U.S. Postal Service and email to contractors and organizations that actively own and operate HDD drilling units. The number of completed surveys allowed for an accurate statistical portrayal of the market. Survey responses came from all 50 states plus Puerto Rico.

Positive vibes

For the last several years, the energy boom has expanded the large rig size of the market and that has trickled down into mid-sized rigs as well. While there has been a market slowdown for energy so far in 2015, other markets for small to large rigs remain vibrant and indeed, growing. Plus, energy should steadily rebound in the near future.

It all adds up to a stable, healthy market that is much coveted by veteran contractors, manufacturers and service companies. Pointed out a contractor from the upper Midwest, “With all of the public road right of ways being filled up with buried utilities the only option left is directional drilling. Plowing in facilities is a thing of the past!”

Another contractor from the eastern U.S. predicts a bright future for their HDD endeavors. “We see the HDD market growing to be the standard for all utilities being installed. Our growth in the Mid-Atlantic area is expected to be about 50 percent more than last year.”

Another contractor is excited about HDD opportunities. “It’s hot through the Midwest. More water installation than in the past.”

Concerns

But with that overall market health emerges the challenges that often accompany such a dynamic. While skilled labor is in short supply across much of the construction market, nowhere is that more pronounced than in the HDD arena where a lack of quality labor has become a strong barrier to growth for companies of all sizes.

Aspiring HDD contractors have flocked to this market with images of steady work and high profits. Of course, reality is much different but the impact of underbidding projects and failing to complete said projects leaves owners unhappy with their HDD experience and damages the market. Indeed, a Texas contractor fears that “the long-term [of HDD] will be determined by the amount of damages inflicted due to operator error and negligence.”

“The market looks good right now. That will bring lots of ‘easy money’ seeking newcomers again to start another cycle of dropping prices (especially in the mini rig market),” cautioned this West Coast HDD contractor. “That has always kept us out of that market other than rock drilling or fuel cell work. Our big rig work has become more centered around offering concept, design/engineering and construction of complicated projects. That has been the way to stay out of low price projects that bring the companies that want – and will – take any job to work.”

Many engineers, not as familiar with the nuances of HDD, will design a project to include or rely upon the technology without proper soils inspection, understanding of HDD’s limitations or needs or without consulting contractors regarding route selection and project planning. Naturally, such action can bring mixed results and frequent change orders, again leaving a bad taste in the mouth of those counting on HDD to be their technology savior on a particular project.

“Lack of proper engineering and design causes owners/engineers to attempt to push all design liability onto the HDD contractor,” observed a contractor from the Southeast U.S.

Complained this contractor: “It’s hard to keep the owners, general contractors and engineers interest on new and demanding installation techniques (i.e. HDD), when they are focusing on only installation costs.”

Other contractors agree that while the markets are currently very strong, they are concerned that when telecom or electric grid construction begins to slow in five to 10 years, the HDD market will stall.

Still, through it all, the technology continues to evolve, become more accepted and has even become a stalwart as a regular solution to underground infrastructure installation needs – just where the market needs and wants to be.

Market size

While the various primary market segment shares for HDD remain constant, the size of specific markets is shifting. Telecom remains the largest segment of the HDD market at 20 percent. That figure has remained relatively constant for several years as the fiber build-out across America continues at a strong pace. Markets slowing down slightly include larger diameter energy pipeline installations and sewer.

The pipeline transmission and gathering market dropped from a 15.1 percent share in 2014 to 13.5 percent in 2015. That small drop was anticipated as U.S. shale oil and gas production has continued to rise. With the geopolitical manipulation of the overall energy market by OPEC, principally Saudi Arabia, a glut of oil and gas has emerged. Fortunately for the domestic markets, that glut is relatively small and expected to be quickly absorbed in the near future. But until then, U.S. shale market drilling has dramatically slowed due to price drops and subsequent pipeline construction projects have slowed as well.

For sewer, the market continues to be limited as maintaining line and grade – while obtainable – still tends to be time-consuming, costly and tedious. And, while sewer markets are finally beginning to improve after several years of a severe depression in spending, the neglect of those markets has reemphasized rehabilitation projects in the short term rather than investing on new projects that could potentially utilize HDD.

The strongest growth market for HDD is gas distribution work, up to 19.6 percent from 17 percent last year. With the multitude of mainline and gathering lines being installed over the past five years combined with improved economic conditions – albeit a subdued growth – demand for gas continues to grow in areas now served by mainline pipelines. Gas distribution lines are needed to take that gas from pipelines to customers. HDD has become a critical component of that growth.

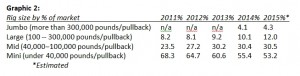

The size of HDD rigs is generally rated by pounds of pullback force and torque. The 2015 survey again reflected that the trend to larger sized equipment continues. The popularity of large rigs (100,000 to 300,000 pullback) has been driven largely by work in the pipeline markets. However, the reasonably compact footprint of these large machines combined with their easy transportability and ability to successfully drill in a broad variety of soil conditions, have made the rigs increasingly popular for other markets such as water.

Mini rigs (under 40,000 pounds of pullback force) remain the single largest market share at 53.2 percent and mid-sized rigs (40,000 to 100,000 pounds of pullback) continue to command a sizable component of the rig market with a 30.5 percent segment share.

Another sign of the times reflecting the strong gas distribution, electric and telecom markets, contractors (52.1 percent) anticipating purchasing slightly more small rigs (under 40,000 pounds of pullback) in 2015. That compares to 50 percent in 2014. Anticipated purchases of both mid-sized rigs (31 percent) and large/jumbo rigs (16.9 percent) by contractors remains relatively constant.

Age of fleet

The overall age of the HDD rig fleet has gone through somewhat predictable variations according to market developments. After the fiber bust of the early 2000s, a virtual freeze on buying new rigs set-in for a few years. The young, new HDD fleet got older as surviving contractors in the HDD field tightened their belts and made existing equipment suffice for many years – even if it sometimes took duct tape and chewing gum. Subsequently, the age of the fleet steadily increased.

But as market conditions slowly rebounded, replacement units began to filter in. There was a period when old rigs were being retired and new units cycled into the fleet at a rapid pace and that led to a younger overall fleet and stability.

For the past several years have experienced strong telecom, electric and gas distribution combined with an increasing focus and need for mid-size and larger rigs. That has led to expansion for many contractors in those fields and the age of the HDD fleet is growing younger again.

HDD rigs still in service that are older than 10 years comprise 20.3 percent of the fleet. Rigs 5 to 10 years old comprise 31.7 percent, units only 2 to 5 years old make up 29.3 percent and rigs less than two years of age account for 18.7 percent.

Drill lengths getting shorter. Modern rigs, tools and accessories and ability for quicker staging and execution of jobs make it more practical and economical for HDD to be used on smaller lengths for common jobs. Improved rock boring capabilities, even in larger rigs, often make HDD preferred over more tedious surface rock breaking and excavation, even for shorter lengths.

While the technology of intersect boring continues to push the envelope for distance with new record lengths set on a regular basis, overall average bore lengths (in non-rock formations) have fallen slightly the past two years. For large rigs, the average boring distance in the last year was just under 2,000 feet, mid-sized rigs drilled an overage of 569 feet and small rigs about 260 feet. As HDD continues to evolve, many drills are more about the capability of the technology than just distance. Barriers to the use of HDD have steadily eroded over the past decade while tooling and equipment continue to improve making once impractical bores realistic.

High density polyethylene (HDPE) pipe continues to be the number one pipe used for HDD work with a 41.4 market share. PVC use continues to slow grow largely due to fusible pipe and enhanced restrained joint technology. Also of note, the “other” category of pipe has expanded as manufactures continue to work with contractors to make more pipe HDD compatible.

What’s important

Each year, the HDD Survey asks contractors what qualities are most important from their HDD equipment/service providers. “Service” continues to dominate with 71.4 percent of contractors highlighting that quality. “Quality” of contractors’ equipment/services providers increased substantially in 2015 as it was selected by 62.5 percent of respondents. Also notable, while cost remains a strong factor in the purchase of HDD equipment, it was highlighted by only 48.2 percent of the contractors.

Purchasing a used HDD rig continues to be a viable option for most contractors. About 62.5 percent of respondents report buying a used rig before, and 55.3 percent state they will strongly consider buying a used rig for their next purchase: 64 percent would consider buying a used small rig; 32 percent of contractors would seriously look at a used rig for the mid-sized market; and 8 percent would look at used HDD units for large or jumbo applications.

In 2014, contractors averaged buying .67 units (all size classes). In 2015, that number is expected to increase to .78. For those contractors who indicated they were going to purchase a rig in 2015, 53.7 percent said it would be a small unit, 38.3 percent a mid-sized unit and 8 percent plan to invest in either a large or jumbo rig.

New contractors continue to enter the HDD market. Some do so simply because they perceive an opportunity. But many established contractors are steadily adding HDD to their repertoire of technologies out of necessity as the popularity and success of HDD rolls on. In fact, 77.8 percent of contractors believe that the HDD market is more competitive today than in the past. A contractor from the mountain states recently invested in HDD equipment based upon market demands. He reports that the HDD market has become “very strong. Now that we have an HDD rig, we find more uses for HDD.”

Said this California HDD contractor about competition: “After being in this industry for approximately 20 years, it strikes me as unbelievable how many companies come and go. It look like easy money from the outside I guess.” Warned a contractor from the Midwest: “Towards the end of 2014, we started to see a new group of start-up HDD contractors enter the market and start driving down unit pricing again. I believe by 2016, we will have another ‘wash-out’ of small contractors because of their lack of understanding in both HDD and small business operations”

A Rocky Mountain state contractor reflected that the HDD market has “unstable prices but stable work availability.”

Rig longevity is always an important cost factor for contractors. How well crews maintain their HDD units and keep them productive is often the difference between long-term profit and loss for contracting companies. Survey respondents report that they generally replace a small rig after 3,850 hours of service; mid-sized units are generally not replaced until after 6,700 hours; and large rigs have major make-overs after 2,700 hours of operation.

For new installations, just how frequently is HDD incorporated into overall construction operation by HDD sub-contractors and general contractors? The survey reported that in 2015, underground construction contractors anticipate using HDD on 48.7 percent of their major projects. By 2020, they expect that number to rise to 56.1 percent. Truly, HDD has become as disruptive a technology as the common backhoe.

On average, contractors that incorporate HDD regularly into their operations own on average 3.9 rigs. Mini rigs owned average 2.9 per contractor, mid-sized rigs owned average 1.7, large rigs owned per contractor is .6 and jumbo rigs owned is .3.

The HDD market has proven to be resilient and innovative. But it’s not for those without dedication and perseverance. “It’s a tough racket. You had better lace up your boots and bring your A game every day if you want to make it in the drilling world,” stressed this Midwest contractor.

Comments